What is DeFi? Well, it stands for Decentralized Finance, a revolutionary concept that’s reshaping how we think about money, investments, and financial services.

DeFi is a term that encompasses a variety of financial applications in blockchain and cryptocurrency aimed at disrupting traditional financial intermediaries.

Decentralized Finance doesn’t require blockchain technology, but it was certainly the catalyst that started the trend. It leverages blockchain technology to remove centralized institutions from financial transactions, offering a peer-to-peer model of conducting business. From borrowing and lending to trading and investment, DeFi opens up a world of possibilities, all operating on transparent, secure, and efficient blockchain networks.

But DeFi comes with complications of its own, such as whether or not the code is open-source (verifiable). You also need to know a bit about how blockchains work to understand how to use DeFi, but we’ll get into all that below. And hopefully one day soon, you won’t need to know anything other than which website to go to or which app to use because it’ll be so easy.

Centralized vs Decentralized Finance

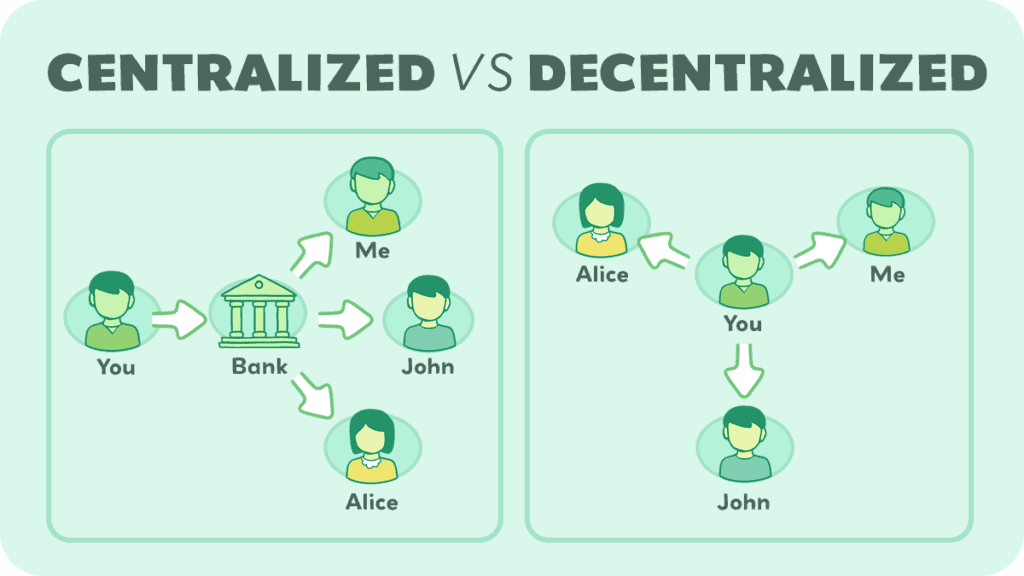

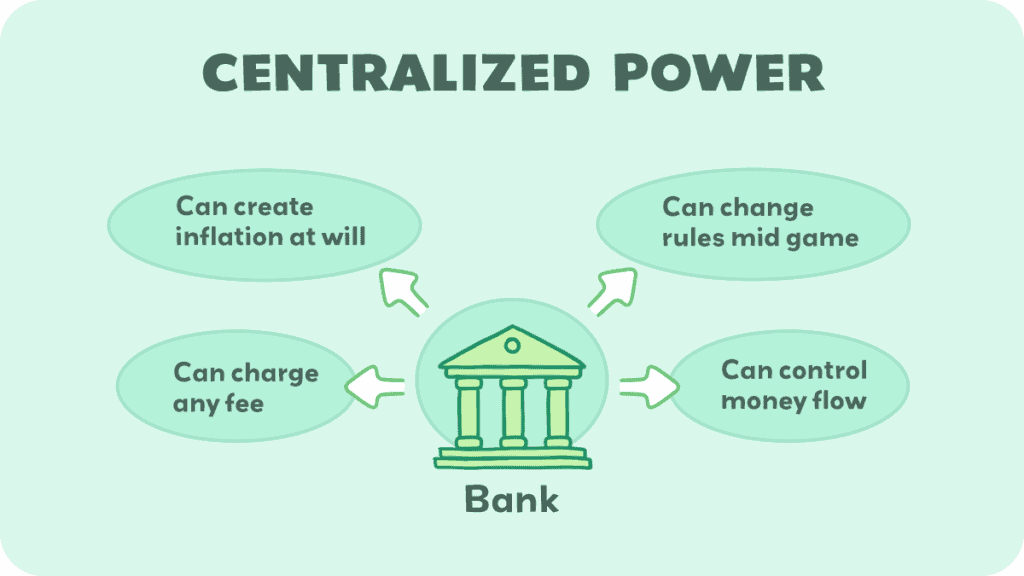

In the past, we have always used centralized finance (CeFi), where there is a central authority that controls the flow of money: the government and the banks.

Centralized institutions can:

- print more money, causing inflation

- stop you from borrowing money

- stop you from having a bank account

- change the value of your money

…and you couldn’t really argue against it because you gave them your money knowing all of this.

Traditional finance is also quite expensive. Payday loans go up to 500%, Credit cards can average 25%, and even personal loans can cost you 18% of your value. These are high rates, but you pay them if you need to because that has been the only option.

But now there are new options.

You’ve probably heard about blockchain and cryptocurrencies like Bitcoin and Ethereum. They’re often in the news for their rising values and the excitement they generate. But there’s another aspect of this digital currency world that’s gaining attention: decentralized finance, or DeFi.

DeFi is a new set of financial tools that operate independently of traditional banks and financial institutions. Imagine a world where you don’t need to go through a bank to get a loan, or where you can invest, trade, and save money without relying on these big companies. That’s what DeFi offers – a financial system run by people and technology, not big corporations.

The magic behind DeFi is blockchain technology. It’s the same tech that makes cryptocurrencies work. A blockchain is a digital ledger that records all transactions securely and transparently. In DeFi, this technology lets you do financial transactions directly with others, without needing a middleman like a bank.

Let’s compare CeFi and DeFi.

| Factor | CeFi (Centralized Finance) | DeFi (Decentralized Finance) |

|---|---|---|

| Accessibility | Requires going through banks or financial institutions, often with geographical and status-based restrictions. | Accessible to anyone with an internet connection and a digital wallet, regardless of location or status. |

| Operation Time/Date | Limited to business hours and days, often excluding weekends and holidays. | Operates 24/7, allowing transactions and activities at any time, including weekends and holidays. |

| Censorship | Subject to regulatory controls and censorship, with institutions having the power to freeze accounts or reject transactions. | Offers a censorship-resistant environment where transactions can’t be easily stopped or altered by a single authority. |

| Cost | Involves fees for transactions, account maintenance, and other services, often higher due to intermediary costs. | Generally lower costs as it removes intermediaries, though fluctuating gas fees on networks like Ethereum can be high. |

| Transparency | Limited transparency; operations and transactions are not public, and the inner workings are often confidential. | High transparency with public blockchain records; all transactions and smart contract codes are visible to anyone. |

| Control Over Funds | Users rely on institutions to manage and safeguard their funds, leading to counterparty risk. | Users have complete control over their funds, though this comes with the responsibility of managing security (like private keys). |

| Intermediaries | Requires intermediaries like banks, brokers, and other financial institutions. | Operates without traditional intermediaries, using smart contracts and decentralized protocols instead. |

| Flexibility and Innovation | Relatively slow to adapt to new technologies and innovation due to regulatory and institutional inertia. | Rapidly evolving, often experimenting with new financial products and services, fostering innovation. |

Decentralized finance is built on three main things that we explain elsewhere, so if you’re interested in the technology side of it, you can check out the links below:

The Evolution of DeFi

DeFi isn’t as new as it seems. It all started with the creation of Bitcoin in 2009. Bitcoin was groundbreaking because it introduced the world to blockchain technology – a way to record transactions in a secure, transparent manner. However, Bitcoin was mainly about transferring digital currency, not offering the full suite of financial services.

The concept of the internet was starting to change. Unlike the current version of the internet (Web 2.0), where data is primarily controlled by centralized entities (like big tech companies), the idea of Web 3.0 began to take hold. Web 3.0 aims to create a more decentralized online ecosystem. It’s a concept for a new version of the World Wide Web based on blockchain technology, which incorporates decentralization and token-based economics.

Ideally, in Web3:

- Users have ownership and control over their own data.

- Transactions and interactions are done directly between users, without needing intermediaries.

- Decentralized applications (dApps) run on blockchain networks, promoting transparency and security.

- Cryptocurrencies and digital assets play a significant role in the economy and functionality of the web.

The idea is to create a more open, trustless, and permissionless internet, where users have more power and privacy, and the digital economy is more inclusive and distributed. It’s not quite clear what exactly Web 3.0 will look like, and there are still a lot of questions to be answered.

Enter Ethereum in 2015. Ethereum took blockchain a step further and set the stage for Web 3.0. It wasn’t just a currency; it was a platform where developers could create their own blockchain-based applications called dApps (decentralized applications).

This was huge because it opened the door to more than just sending and receiving digital money. Now, people could build all sorts of financial apps on the blockchain, laying the foundation for what we now call DeFi.

The real growth of DeFi started around 2018. This is when we began seeing a surge in DeFi applications, thanks to Ethereum’s flexibility. These applications included lending and borrowing platforms, decentralized exchanges, and more. They allowed people to do things with their crypto assets that were previously only possible through traditional financial institutions.

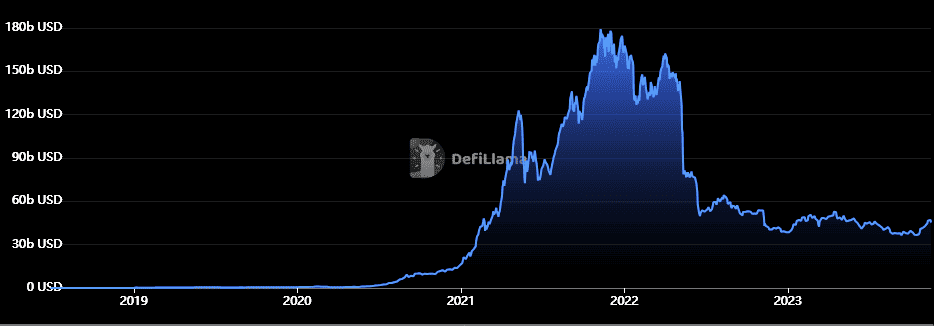

Take a look at the spike in popularity late 2021:

Fast forward to today, and DeFi has exploded in popularity. It’s not just a few tech enthusiasts using these services anymore. Now, it’s attracting attention from regular folks and even big investors.

The total value locked in DeFi – basically, the amount of money flowing through these applications – has skyrocketed to over $46 billion USD as of November 2023, showing just how much people are embracing this new way of handling their financial affairs.

At peak hype, there was over $200 billion in DeFi protocols:

What’s so special about this growth? It shows that people are looking for alternatives to traditional finance. They want more control, better access, and less dependency on big institutions.

DeFi’s history is not just about technology; it’s about a shift in thinking, about people wanting a more open, accessible, and fair financial system.

Not to mention, Web 3.0 and DeFi are revolutionizing how we interact with the digital world in general. Everything from art to music to games and the Metaverse are all operating on the blockchain now.

Sidebar: What is the Metaverse?

The Metaverse refers to a collective virtual shared space created by the coming-together of virtually enhanced physical reality, augmented reality (AR), and the internet. For instance, you may be familiar with the “old-school” metaverse called Second Life, which has its own unique culture, currency, and marketplace. Blockchain takes this to the next level. In the blockchain world, the Metaverse is often a network of 3D virtual worlds focused on social connection, underpinned by decentralized technology.

Blockchain technology enables true digital ownership in the Metaverse. Through NFTs (Non-Fungible Tokens), users can own unique digital assets like virtual land, avatars, outfits, and art. These assets are secured on the blockchain, providing proof of ownership and authenticity. And they can even be traded with other players!

Key DeFi Terms

Before we get too far into it, we want to make note of some important terms and concepts you’ll need to know as you continue to read this article. We have a separate glossary, if you come across a term that isn’t on this list, but we’ll do our best to include the most important definitions here.

| Key Term | Definition |

|---|---|

| Public Address | A publicly visible identifier, similar to an account number, used to receive cryptocurrency transactions. |

| Private Key | A confidential code known only to the owner of a digital wallet, used to access and manage cryptocurrencies. |

| Self-Custody Wallet | A type of digital wallet where the user holds and controls their private keys, giving them full control over their assets. |

| Custodial Wallet | A wallet where a third party, like an exchange, holds the private keys, meaning they have control over your assets. |

| Lending | The act of loaning your crypto assets to others through a DeFi platform, often in return for interest payments. |

| Borrowing | The process of taking out a loan in cryptocurrencies from a DeFi platform, usually by providing other crypto as collateral. |

| Trading | The buying and selling of cryptocurrencies or crypto-based assets, often done on decentralized exchanges (DEXs). |

| Yield Farming | A strategy where users lend or stake their crypto assets in a DeFi protocol to earn more cryptocurrency as rewards. |

| Liquidity Pool | A collection of funds locked in a smart contract, used to facilitate trading on a DEX by providing liquidity. |

| Stablecoin | A type of cryptocurrency that is pegged to a stable asset, like the US dollar, to maintain a consistent value. |

| Coin | A digital currency that operates on its own blockchain, primarily used as a medium of exchange or store of value. They are needed for the blockchain to function and are often used as gas (see below). |

| Token | A digital asset created on an existing blockchain, representing assets or utility within a specific ecosystem. Can include “currencies” or “NFTs“. |

| Governance Token | A cryptocurrency that gives holders the right to vote on decisions affecting the future of a DeFi platform or protocol. |

| Smart Contract | A self-executing contract with the terms of the agreement between buyer and seller being directly written into lines of code. |

| Decentralized Application (dApp) | An application built on a decentralized network that combines a smart contract and a frontend user interface. |

| Gas Fees | The fees paid to conduct a transaction or execute a contract on a blockchain network, particularly in Ethereum-based DeFi. |

| Impermanent Loss | The temporary loss of funds experienced by liquidity providers in a liquidity pool due to volatility in the price of assets. |

| On-board | Swapping fiat for crypto, usually through an exchange. |

| Off-board | Selling crypto for fiat, usually through an exchange. |

Key DeFi Systems

There are several important components of DeFi systems that make them function the way they do. Everything from the base blockchain layer to the thousands of cryptocurrencies that work on them.

Let’s take a brief look at the most important parts.

Blockchains

First up, we have blockchain technology. This is the backbone of DeFi. Remember, blockchain is a digital ledger that’s transparent, secure, and can’t be tampered with. It records every transaction that happens in the DeFi space. Just like a ledger in a bank, but accessible to everyone and much more secure.

If you want to view the activity on a blockchain, it’s easiest to use a blockchain explorer, such as EtherScan.io. They look daunting at first because they have a lot of data, but we recommend taking a look through it just to get familiar with it, as it will help you a lot in tracking your own assets, doing research, and even in identifying scams.

Smart Contracts

Next are smart contracts. These are automatic agreements written in code on the blockchain. When certain conditions are met, these contracts automatically execute the terms of the agreement.

For example, if you’re lending money through a DeFi platform, a smart contract will ensure you get your interest payments without anyone needing to process it manually.

dApps

Then, there are decentralized applications (dApps). These are the apps built on the blockchain that let you interact with DeFi services.

Whether it’s borrowing, lending, or trading, dApps are your gateway to these services. The cool thing is, they’re not controlled by any single entity – they’re powered by smart contracts, making them transparent and trustless.

DEXs

One key element in the DeFi ecosystem is Decentralized Exchanges (DEXs). Unlike traditional exchanges where trades are managed by a central authority, DEXs allow you to trade directly with others on the network. This means lower fees and no need for a middleman.

Crypto Coins and Tokens

Last but not least, we have cryptocurrencies. These digital assets represent a wide variety of value and rights within the DeFi ecosystem. These include stablecoins that are tied to the value of real-world assets, like the dollar, to governance tokens that let you vote on how a DeFi platform should be run. There are actually many kinds of tokens, so let’s get into it.

Coin vs. Token

First, the difference between a coin and token. As we said in the glossary, a coin is a digital currency that operates on its own blockchain, primarily used as a medium of exchange or store of value. They are needed for the blockchain to function and are often used as gas. An example of a coin is ether (ETH) on Ethereum.

On the other hand, a token is a digital asset created on an existing blockchain, representing assets or utility within a specific ecosystem. This can include “currencies” or “NFTs“, or any number of other tokenized asset such as real estate ownership documents or tokenized bonds.

Soulbound Tokens

Soulbound tokens are a concept in the blockchain world, representing non-transferable tokens. These tokens are tied to one wallet and cannot be sold or transferred to another. Here’s what makes them unique:

- Identity and Reputation: Soulbound tokens can represent a person’s identity, qualifications, affiliations, or achievements within a blockchain network. For example, a token might indicate completion of a certain course or membership in a club.

- Non-Transferable: Unlike regular tokens, which can be traded or sold, soulbound tokens are permanently linked to a single wallet. They are more about representing personal attributes or achievements than monetary value.

- Use Cases: These tokens could be used for various purposes like verifying credentials, building trust in decentralized finance, or creating a more robust digital identity system.

Wrapped Tokens

One kind of token we haven’t touched on yet is the wrapped token. A wrapped token is a token on a blockchain that isn’t its native blockchain. For instance, if you want to use ETH on the Polygon blockchain, you would need to use wrapped ether, or wETH). ETH is native to the Ethereum network, not the Polygon network, so in order to be on Polygon it needs to be “wrapped”. The process is basically when someone bridges ETH to Polygon, the bridge burns the ETH on Ethereum and mints wETH on Polygon. This way, the value of ETH is the same across chains and the wETH replaces the ETH, rather than duplicate it.

Wallets

One of the most important things everyone needs to know about DeFi is how to use wallets. Wallets are the means through which we use crypto, buy NFTs, even play blockchain games. They are the unique identifiers of individual addresses.

One example of a popular wallet is Metamask, which operates on networks built with the Ethereum Virtual Machine (EVM), such as Arbitrum, Optimism, Polygon, Aurora, and Binance Smart Chain. Metamask, and many other wallets, are both browser extensions and phone apps. When you set it up, you create a new wallet and are given a secret recovery phrase, which is crucial for accessing your wallet if you forget your password or change devices. You NEVER want to give out this secret recovery phrase, also called a seed phrase, because whoever has it has complete control over your wallet.

Metamask acts as a digital wallet where you can store Ethereum (ETH) and other Ethereum-compatible tokens (like ERC-20 tokens). It’s like a bank account for your digital currency. With Metamask, you can easily send and receive cryptocurrency. You simply enter the recipient’s wallet address to send crypto or provide your address to receive it. One of the key features of Metamask is its ability to interact with decentralized applications (DApps) on the Ethereum blockchain. This means you can use Metamask to participate in DeFi platforms, trade tokens on decentralized exchanges, collect NFTs (Non-Fungible Tokens), and more.

Metamask released a new feature recently that makes it more versatile, called Snaps, which allows Metamask to extend its capabilities beyond just managing cryptocurrencies on Ethereum and EVMs. So, for instance, users can now access the Solana blockchain on Metamask, or they might be able to connect with dApps in new ways. Keep in mind though that these Snaps can be community developed, so they aren’t necessarily safe.

Metamask is just one example of a crypto wallet. There are many of them, and they all have similar features, but different interfaces. As ever, there are a lot of scam wallets too though so make sure you are using one that is trusted and well-known. You can usually find a list of verified wallets on the blockchain’s own website, such as the test to find what Bitcoin wallet is best for you on Bitcoin.org. Remember, most wallets only support one blockchain, or group of blockchains, so be careful with what you’re using and how you’re wanting to use it.

Wallet Safety

We’ve mentioned safety a few times, so let’s get into some specifics. Wallet safety is crucial in managing your cryptocurrencies and interacting with blockchain networks because they are your only reasonable means to do anything in DeFi.

Types of Wallets:

- Hot Wallets: These are connected to the internet, like those in exchanges or apps like MetaMask. They’re convenient for frequent trading and transactions but more vulnerable to online threats.

- Cold Wallets: Hardware wallets or paper wallets, not connected to the internet, suitable for long-term storage of crypto. They’re less convenient for frequent transactions but much safer.

Keeping Your Wallet Secure:

- Secure Your Private Keys: Never share your private keys or seed phrase with anyone. This is like the key to your bank vault – if someone gets it, they can access your funds.

- Use Strong, Unique Passwords: For wallets that require a password, ensure it’s strong and unique. Consider using a password manager.

- Two-Factor Authentication (2FA): Enable 2FA for an additional layer of security, especially on wallets or exchanges that support it.

3. Being Cautious with Transactions:

- Double-Check Addresses: Always double-check the recipient’s address when sending crypto. Transactions are irreversible.

- Beware of Phishing: Be cautious of emails or messages claiming to be from wallet services or exchanges. Don’t click on suspicious links.

- You can use an extension called Fire that will pop up any time your wallet is triggered to tell you what the transaction will do and if it’s from a recognized scam address. It’s not perfect, but it helps a lot.

4. Backup Your Wallet:

- Backup Your Seed Phrase: Write down your seed phrase and store it in a secure and private location. Some people use safes or safety deposit boxes.

- Consider Multiple Backups: Having more than one backup, ideally in different physical locations, can be a safeguard against loss due to disasters like fire or flood.

5. Using Wallets Wisely:

- Regularly Update Software: Keep your wallet software up to date to ensure you have the latest security enhancements.

- Be Informed: Stay updated on the latest security threats and best practices in cryptocurrency security.

DAOs

A DAO, or Decentralized Autonomous Organization, is like a company or a group that runs entirely on blockchain technology, without any central authority. Decisions in a DAO are made by its members, who typically vote on important matters using tokens. It’s a democratic way of managing an organization, where everyone’s voice can be heard.

DAOs play a crucial role in the DeFi world. Many DeFi platforms operate as DAOs. This means that users of the platform can have a say in how the platform evolves. For instance, if a DeFi platform wants to change a rule or introduce a new feature, its community can vote on the decision. This approach ensures that the platform operates in a way that aligns with the interests of its users.

DAOs have also transformed how projects raise funds and how people invest. In traditional finance, investment decisions are often made by a small group of people in charge. In DeFi, through DAOs, a larger community can pool funds together and decide collectively on investments. One of the ways that funds are gathered is through quadratic funding.

Quadratic Funding

Quadratic funding is a method of funding public goods (like open-source projects, community initiatives, etc.) that optimizes for the preferences of the community rather than the preferences of a few wealthy individuals or entities. It’s designed to democratically determine the allocation of funds to projects based on the number of supporters rather than the amount donated.

Imagine a scenario where several projects need funding, and a community of people decides which projects get how much. In quadratic funding, the amount of funding a project receives isn’t just based on the total money it gets from supporters, but also on the number of supporters it has.

Here’s a simple way to understand it: If ten people each donate $1 to a project, that project might end up getting more funding from the quadratic funding pool than if one person donates $10. This system values the width of support (how many people support) more than the depth of support (how much money is given).

Popular DeFi Services

Okay, so now you understand that DeFi has a lot of parts to it, and all of them end up working together to make the DeFi ecosystem work.

Why use DeFi? This question might sound redundant by now. You know that DeFi is revolutionary when it comes to money. But there’s also another people want to use DeFi, and that is to make money. Whether you’re getting the rewards from lending and borrowing, or doing more active day-trading, DeFi is a popular way to not only use money as a form of value exchange, but also as a form of investment.

Let’s zoom in on the types of DeFi applications that exist and how to use them.

Exchanges

The first thing we need to look at is exchanges. Why? Because they are how people get crypto. We mentioned already that there are two types of exchanges: centralized and decentralized.

Let’s look at an example to help understand the difference. I have a friend who traveled to London a few years ago from the US. Of course, in London, the standard currency is the pound, while over here in the US, it’s dollars. So naturally, he had to visit a foreign exchange booth and trade out his dollars for pounds.

Unfortunately for him, the fee was like 15%, so he immediately lost 15% of his money. Foreign exchanges take advantage of tourists who don’t know any better, or don’t have other options, and they need local money.

This is an example of a non-crypto, centralized exchange. There are centralized exchanges (CEXs) that trade in crypto too, such as Coinbase or Binance. They usually have fairly high fees because that’s how they make money. Most people will “on-board” to crypto using a centralized exchange because it’s much easier than having to learn how to use a decentralized exchange (that is changing though!).

Most importantly about centralized exchanges: never keep your crypto on an exchange! Why? Because you don’t control it, they do; it’s basically the same as a bank. You’ll want to transfer your funds to a self-custody wallet, which we’ll get into a little later.

This is why we call CEXs “crypto banks” – they are no better than keeping your money in a traditional bank because they still control the assets.

Directly on-boarding to crypto using a decentralized exchange (DEX) has been challenging. Until recently, there wasn’t really a good way to do this that was guaranteed to be safe. But that is, thankfully, changing.

Why would you want to use a DEX? There are usually very small fees, like less than half a percent, which is really important for anyone who regularly wants to trade their crypto assets. They also only require the one step of purchasing the crypto, whereas if you use a CEX, you need to purchase it and then send it to your own wallet, which adds extra fees. You also can’t be sure that the CEX will give you the assets you bought, or that they will send it on the right network, whereas with a DEX you are doing it all yourself so it’s sure to be the right thing.

CEXs tend to pool user funds, so while it looks like you have your own wallet, you don’t really, they’ve just assigned you a wallet address. It’s also not always clear which blockchain the asset is on. For instance, you can buy ETH but the exchange might be holding it on the Polygon network because it has lower fees than the Ethereum network. So when you try to send it to your personal wallet, this can be a little tricky.

Most popular decentralized exchanges, or DEXs, work in a manner where investors pool their money together and then traders can trade that money. For instance, if you want to exchange ETH (ether) for OP (optimism), there will be a pool of both coins that other people have put together so that you can trade it automatically.

The fee for each trade goes to the pool investors, and the amount is set in advance. It’s also all written in code, so it can’t change. A government can’t step in and say, “You can’t buy bitcoin anymore,” because the code can’t be blocked. (It can be sanctioned, but that’s a story for another post.) This is why we have the saying, “code is law.”

Decentralized Exchanges open the world up to a whole new variety of tokens and coins.

For example, Coinbase, the first centralized exchange to go public, only allows you to buy and sell a limited number of cryptocurrencies. Since they are regulated by the government and have to abide by certain rules, they closely analyze each coin before adding it.

On the other hand, the most popular decentralized exchange, Uniswap, has literally thousands of tokens that you can trade, and they aren’t regulated by anyone. That’s the decentralized part; there are billions of dollars locked up in these liquidity pools so traders can trade, but nobody can control these billions of dollars… they are just following a program that someone wrote.

In fact, only investors could be the ones to pull their money out of the pool, but then lending rates would rise and new investors would come along.

Remember, there are small fees in DEXs that are paid to the lenders. A lending rate is the percentage of fees each person lending their money to the pool receives. The more people are in the pool, the lower the percentage of fees each one will receive.

So, basically, there are centralized and decentralized exchanges. A CEX holds your funds so you don’t always have control, but a DEX keeps the funds under your control. You can make money by providing cryptocurrencies to lending and borrowing pools on DEXs, or just use them as a way to swap crypto.

Bridges

Okay, so you know how to get crypto through exchanges. But how do you move it around?

Remember how we said the CEX might not always have the asset on the network you want it on? Well, to get it to the right network, you’d use something called a bridge.

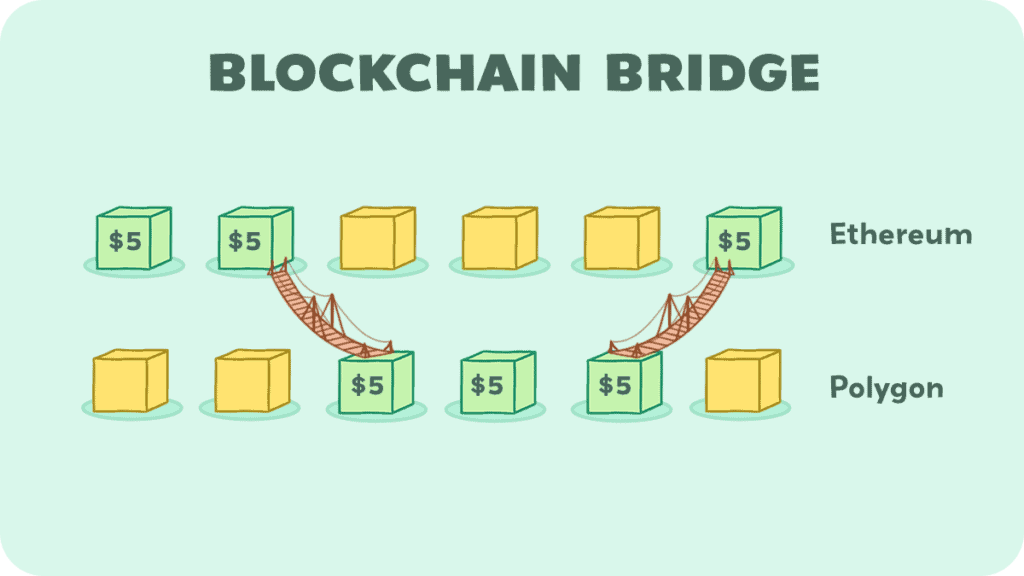

Crypto bridges, also known as blockchain bridges, allow you to transfer assets and information between different blockchain networks. Since blockchains are typically independent and cannot communicate with each other directly, bridges serve as a crucial connection.

For example, if you have a token on the Ethereum blockchain but want to use it on the Binance Smart Chain (BSC), a crypto bridge can help you convert that token into a format compatible with the Binance Smart Chain. The bridge ensures that the value is transferred correctly and securely between the two different blockchains.

Crypto bridges enhance the interoperability and flexibility of different blockchain networks, making it easier to use various blockchain services and applications regardless of the underlying blockchain infrastructure.

In order for the bridge to work, it needs coins or tokens on both networks already, in what are called liquidity pools. Anyone can lend their assets to bridge pools to get paid interest by user fees, since everyone who uses a bridge pays a small fee for it. There are also liquidity pools for simple swaps on DEXs.

Most of the time, people lend two or more assets to a liquidity pool. To go back to our bridge example above, if someone wants to move ETH from Ethereum to BSC, the bridge needs to have ETH on Ethereum and wrapped ETH on BSC. So a person who is lending their assets to the pool would lend both ETH and wETH to allow this trade to happen.

But it is possible to provide single-sided liquidity. In a single-sided liquidity pool, you only need to deposit one type of asset. This reduces the complexity and risk for those who want to participate in providing liquidity, because they don’t have to worry about keeping two or more assets’ value balanced. The problem that arises with this is if there is more of one asset than another, then the trades won’t all be able to occur. So, it’s better for the lenders than the users.

Lending/Borrowing

Okay, let’s get into lending and borrowing. A huge part of our traditional financial situation is based on lending and borrowing money, but the blockchain can do it better. Why?

One of the reasons we can reliably lend and borrow with banks is because the government can hold both us and the banks accountable. Imagine you take out a loan from a bank to buy a car. The bank agrees to lend you the money, and in return, you agree to pay back the loan with interest over a certain period.

If you fail to make the payments, the bank can take legal actions like reporting the failure to credit bureaus, seizing the car (if it was used as collateral), or suing you to recover the money. If the court rules against you, you might be required to pay the debt by automatically taking part of your paychecks, or by them seizing your other assets, like a house.

On the other hand, one of the agreements you make with a bank is when you store your money there, they can use it to give other people loans, but you’re supposed to be able to take it out any time. Actually, it has happened a few times in history where the banks aren’t able to hold up their end of the deal, so the government has to step in so people can get their money back.

You can see how the traditional system can be beneficial when it comes to protection of loans. In the new world of DeFi, there is a lack of this kind of security because one of the pros of crypto is anonymity; no one can make you pay back a loan if they don’t know who you are.

The good news is we have found a way to solve this. With the use of smart contracts, we can actually allow others to use our funds, while still keeping custody of them.

Let’s look at an example.

Alex has some cryptocurrency and wants to earn extra money from it. Bailey wants to borrow some cryptocurrency. Alex can use DeFi platforms like Compound or Aave to lend his coins. He puts them in a smart contract and gets special tokens (CTokens or ATokens) that show he’ll get his coins back with extra money (interest). When Alex wants his coins back, he just swaps his special tokens in the smart contract, and it automatically gives him his coins plus the extra interest.

For Bailey to borrow, she needs to give more cryptocurrency as a promise (we call this over-collateralizing). Let’s say she wants to borrow $100, but she has to promise $120 worth. If Bailey doesn’t pay back, the smart contract uses his extra promised money to pay Alex back.

Okay, hopefully that’s clear. The smart contract will automatically balance the pool to make sure the lender (Alex) can get their money back. But, you might be asking why Bailey would borrow if she already has money?

Well, imagine you have ether coins you think will be worth more later, but you need some cash now. You can use your ether as a promise, borrow some stablecoins like Tether, and use that money now. Later, you pay back the loan and get your ether back, which might be worth even more now!

But what if you don’t make enough money to pay back the full loan? You can either add some more money to pay it all back or just keep what you made and let the lender keep your Ethereum.

There’s also something called a Flash Loan in crypto. This is super quick, like 10 seconds! It’s used for making money by automatically buying and selling fast, like buying ether cheap on one platform and selling it for more on another.

But be careful – a lot of crypto scams work with flash loans. They say they have a flash loan bot that will make sure this works, but the bot actually won’t give you the money back. Plus, the more bots there are, the less likely it is to work because they are all competing to be faster than the others. If someone has a bot that works, why would they give it to other people? Wouldn’t they want to make the money themselves? So definitely watch out for this common crypto scam.

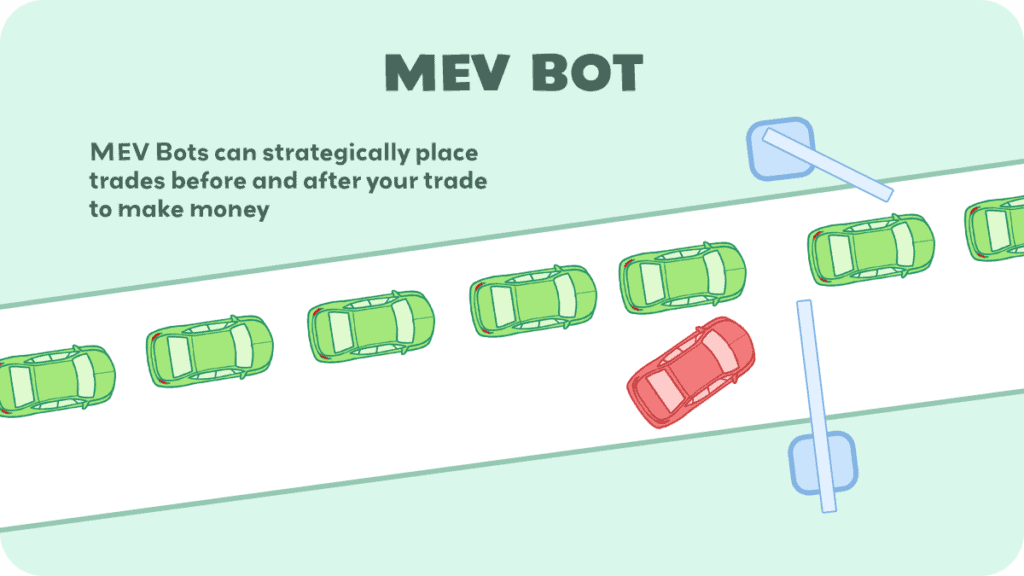

Another kind of bot to look out for are MEV bots. MEV stands for “Miner Extractable Value.” MEV bots focus on the list of transactions that are not yet confirmed (called the mempool) and put into a block on the blockchain (if that doesn’t make a lot of sense to you, please read our “What is a Blockchain?” post).

How MEV bots operate is kind of complicated, but most simply, they watch all the transactions waiting to happen and look for chances to make a profit. For example, they might find a way to buy something at a low price in one place and sell it for a higher price somewhere else (called arbitrage). Or they might find transactions where they can step in and make money due to changes in prices (sometimes causing liquidations). And they also perform sandwich attacks, which is placing transactions before and after a targeted transaction to profit from the price movement caused by the targeted transaction.

MEV bots can significantly affect the network and its users. While they provide liquidity and efficiency in some cases, they can also lead to negative impacts like increased network congestion and unfair advantages. Their actions might also result in worse trades for regular users. So, blockchains like Ethereum are working to limit the ability of MEV bots to operate.

Margin + Synthetics

Margin trading is a whole new beast. Let us explain margin trading in the traditional world real quick, then we’ll explain it in the decentralized world.

Okay, so you want to buy Apple stock, and right now it is at $100. Essentially margin is a loan that will automatically sell your stock if it goes below your down payment. So to buy that $100 stock, you need a $100 loan, and the bank agrees to give you a $100 loan if you can give them a $20 down payment and a small fee of 5% a year.

Here are two scenarios that could happen:

Scenario 1 – Stock Increases in Value

The stock goes from $100 to $150. You decide to sell the stock, so you get $150, pay back only $80 of your loan – because the bank already had your other $20 as a down payment, and keep the rest, which is a profit of $70.

Essentially you made $70 by only spending $20. This means you more than tripled your money. This is the power of margin, you use margin when you think something is going to increase in value to multiply your own money.

Scenario 2 – Stock Decreases in Value

Now, this is the second scenario, and it’s if the stock drops in price. Well, with margin… you actually have to sell as soon as the value of what you bought can’t pay back your loan.

So the stock starts at $100, then drops to $90, then $85, then once it hits $80… boom, the bank FORCES you to sell your Apple stock so you can pay them back the $80 you borrowed. So the $80 you made from selling the stock plus the $20 you gave them as the down payment equalizes the loan and the bank has the $100 they originally gave you. You have paid your loan back… but you didn’t profit anything. In fact, you lost your original $20.

In CeFi, to trade on margin you usually need three things: 1) to be able to prove who you are, 2) have a minimum of a few thousand dollars, 3) pay fees that are usually higher than 5%. Also, they only work on “bank hours”, which is usually weekdays between 9 AM and 5 PM.

In DeFi, margin trading can be a lot quicker because it’s available at all times, open to anyone anonymously with any amount of money, and it’s safer as well because it’s all coded in so you don’t have to rely on anyone holding up their end of the bargain.

Okay, so that’s margin, but what is synthetics?

Synthetics in DeFi are a bit like having a virtual copy of something real. They are special kinds of tokens that represent other assets, like gold, stocks, or even other cryptocurrencies, but you don’t actually own the real asset.

For example, a synthetic token might track the price of gold. If the price of gold goes up or down, so does the value of your synthetic token. It’s a way to invest in different assets without actually having to buy them.

Yield Farming

Yield Farming is a popular way to earn extra cryptocurrency in DeFi. Yield Farming is when someone lends their crypto in order to make profit from the interest rewards.

The reason it’s called “farming” in the active, continuous sense is because usually yield farmers hop between lending pools to get the highest reward rate. Remember how we said earlier that the rewards are based on how many people are in the pool? Yield farmers try to keep moving to keep up with the highest rates.

Let’s use an example to make this clearer. Imagine Jordan has some ETH. Jordan decides to use his ETH in Yield Farming to earn more crypto. He finds a DeFi platform, let’s call it “GrowCrypto,” that offers Yield Farming.

Here’s how it works:

- Jordan Lends ETH: He lends his ETH to GrowCrypto’s platform.

- GrowCrypto Uses the ETH: The platform then uses Jordan’s ETH to help other people trade, lend, and borrow.

- Earning Rewards: In return for lending his ETH, Jordan earns rewards. These rewards are often in the form of other cryptocurrencies.

The cool part about Yield Farming is the potential for high rewards. But there are risks. The value of the rewards can go up and down. Plus, there’s the risk of the platform itself facing issues such as hacks. And a lot of crypto scams are based on promises of “15000% APY!” If it sounds too good to be true, it probably is.

Wait, what’s APY? APY (Annual Percentage Yield) is a measure of how much you earn from an investment in a year, taking into account the effect of compounding interest. In the context of DeFi and yield farming, APY tells you how much you can expect to earn on your crypto investments over the course of a year.

Another term you might hear is APR (Annual Percentage Rate). Unlike APY, APR doesn’t include the effects of compounding within a year. It’s simply the annual rate charged for borrowing or earned through an investment. In DeFi, APR is often used to describe the interest rate you’ll get for lending out your crypto or the rate you’ll pay for borrowing.

Degen Yield Farms

If yield farms aren’t crazy enough, there’s an even riskier type of yield farm called “degen yield farms.”

Degen yield farms, short for “degenerate yield farms,” are a type of high-risk, high-reward investment in the DeFi space. They offer very high returns (or yields) on your investment, but they also come with a much higher risk compared to other types of investments.

In degen yield farms, you usually lend your cryptocurrency or provide liquidity to a new or less-established DeFi project. In return, you earn rewards, often in the form of new tokens. These projects can offer very high returns, sometimes even double or triple digits, but there’s a catch. They are often untested, may have less security, and can be more vulnerable to market fluctuations and other risks.

Two of the most important questions to ask when yield farming, whether degen or not, are:

- Where is the money coming from?

- When should I pull my money out?

Where is the money coming from?

It’s all fine and dandy to get essentially free money, but you need to know where the money is coming from. Usually, it’s being paid by people who use the platform, just like we said earlier about user fees being distributed to liquidity providers, this is basically the same thing.

But sometimes the money is coming from the platform itself as an incentive to use it. For instance, a new DeFi platform might pay you in their token for providing ETH. Their token might be worth a lot, or it might not be, so you have to be careful about what you’re agreeing to.

And always remember that if it sounds too good to be true, it probably is. No one can sustainably pay out 15000% APY. I remember when the Aurora network started in 2022 and the Rainbow bridge that was built for it was giving out crazy APYs, like in the multiple hundreds. But that only lasted for less than 48 hours because so many people started providing liquidity that the percentage had to get spread out more until it was almost nothing.

Which brings us to the next question…

When should I pull my money out?

Trying to time the market is (almost) always a bad idea. No one can predict with any measure of certainty when something will stop making profit, or when it will hit an All Time High. And past action does not guarantee future action.

There’s a style of investing called Dollar-Cost Averaging (DCA). This approach involves regularly investing a fixed amount of money, regardless of the market’s ups and downs. It’s a popular strategy to reduce the impact of volatility on the overall purchase of assets.

Our suggestion, based on Taiki Maeda’s Humble Farmer Thesis, is to do this in reverse – rather than pulling out all your money at once, take it out in a series of withdrawals over time. This might not always be feasible, but if everyone tries to pull their money out all at once, the platform could crash entirely, or it could make gas fees go crazy, or the automatic balancing that happens could wipe out everyone’s lending and borrowing deals.

Just like our example of the government being able to protect people using banks but not crypto, no one can stop the automatic actions of the coded platforms. There isn’t usually insurance on DeFi investments… but there is the idea of insurance in DeFi too.

Insurance

Insurance is really easy to explain. For example, with car insurance, you pay $100 a month to protect your new Tesla. However, one day while using the autopilot feature, another car causes the autopilot to glitch and you drive into a ditch, unharmed… but totally wreck the car.

Well, since you paid insurance, the insurance company pays you what the Tesla was worth so you can go buy a new one. They use statistics to predict how many of their drivers will crash their cars, and use this data to predict how much they would have to pay out each year to determine what the monthly price of the insurance is (which is also called the premium).

Well, with decentralized finance, the insurance company can be code. Let’s say a farmer wants to buy crop insurance so if his crops die he still has income.

We could write a piece of code on the Ethereum network that says, “If there’s any days this summer that are 95 degrees or hotter 4 days in a row, pay out Farmer Joe $100,000. However, he has to pay $2000 to initiate this contract.” So Farmer Joe can buy his crop insurance through a smart contract which would guarantee the payout under the specific conditions.

You might have two questions: 1) How does the code know if it is 95 degrees, and 2) where does the $100,000 come from?

Well, to connect the real world to the blockchain, we have to use something called oracles, which are trusted sources that give the blockchain information. We can create an oracle in our city that reads the temperature and is verified by a few people to make sure it can’t be faked. Then the smart contract can reliably use it as a data source to decide if the insurance requirements are met.

Secondly, the $100,000 comes from other people buying insurance that bought their premiums, but did not need the pay out because the requirements were not met. People can be incentivized to provide this money to the insurance protocol the same way liquidity providers are—with interest paid to them over a period of time.

You might be asking how we can guarantee that the insurance pool has $100,000 in it, especially since cryptocurrencies are not always worth the same amount of money. If someone puts in $100k of ETH, six months later it might be worth $50k, or $200k. Well, this can be solved through something called stablecoins.

Stablecoins

Stablecoins are a unique type of cryptocurrency designed to have a stable value, unlike other cryptocurrencies that can be quite volatile. They are crucial in the DeFi space because they offer the benefits of digital currency without the wild price swings.

One common way stablecoins maintain their stability is through backing by reserves. For example, the USDC Coin is pegged to the US Dollar, meaning for every USDC in circulation, there’s an equivalent amount of US Dollar held in reserve. This one-to-one reserve backing helps keep its value stable.

Another method is using algorithms. Some stablecoins, like DAI, use smart contracts to manage their supply. If the value of DAI starts to rise above a dollar, the smart contract will create more DAI to bring the price down. If the value drops, it reduces the supply to push the price back up. This self-regulating mechanism ensures stability, but can also be quite risky. This is also called “rebasing“, and many tokens other than stablecoins are also rebasing tokens.

Collateral-backed stablecoins are another type. These stablecoins, like MakerDAO’s DAI, are backed by other cryptocurrencies. Users deposit their crypto assets (like ETH) into a smart contract as collateral to generate DAI. This method also helps maintain a stable value by ensuring there’s always backing for the stablecoins in circulation.

Sometimes, stablecoins aren’t so stable, though. As you can see, there isn’t a single way for them to be balanced, and since some of them are backed by reserves off-chain (such as in banks), the transparency we like in crypto is not there. Let’s look at a specific example of a stablecoin being very badly managed.

Terra (UST) was an algorithmic stablecoin, which means it maintained its value through a complex mechanism using smart contracts, rather than being directly backed by a reserve of other assets. Its stability was closely tied to another cryptocurrency, Luna. The system was designed so that if Terra’s value fell below $1, Luna would be used to buy and burn Terra, reducing its supply and theoretically pushing its value back up to $1.

However, in May 2022, this mechanism faced a major crisis. A large amount of Terra was suddenly sold off, which significantly dropped its price. The system responded by creating more Luna to buy back and burn Terra, aiming to restore its peg to the dollar. But this created an oversupply of Luna, which drastically reduced its value.

As Luna’s value plummeted, confidence in the system eroded rapidly, leading to further sell-offs in both Luna and Terra. This created a negative feedback loop. The more Terra’s price dropped, the more Luna was created to compensate, which further devalued Luna. Eventually, both cryptocurrencies lost nearly all of their value, resulting in significant financial losses for investors.

As you can see, even something meant to be stable and risk-free is never actually risk free. Whether you’re in CeFi or DeFi, there is always risk associated. And right now, there are more risks in DeFi because of how unregulated it is, and how new it is. The debate around whether or not to regulate DeFi is ongoing, and most people think that DeFi can regulate itself; right now, it’s just too new and all the kinks haven’t been worked out.

Let’s look at some of the risks, and then dive into the ways we can regulate—internally or externally—the DeFi landscape.

Types of Crypto Investments

There are various methods of investment in the cryptocurrency market, each with its own level of complexity and risk. We’ve mentioned some of them already, but we’ll get into specifics here.

Here’s an overview of some common methods:

| Investment Method | Description | Risk Level |

|---|---|---|

| Buying and Holding | Also called “hodling”, this is purchasing cryptocurrencies to hold in your wallet, hoping their value increases over time. | Low to Moderate |

| Trading | Actively buying and selling cryptocurrencies on exchanges to profit from price fluctuations. Includes day trading, swing trading, and position trading. | Moderate to High |

| Futures Contracts | Agreements to buy or sell a crypto asset at a predetermined future date and price, used for hedging or speculation. | High |

| Perpetual Contracts | Similar to futures but without an expiry date, allowing positions to be held indefinitely with margin requirements. | High |

| Short Selling (Shorts) | Borrowing a cryptocurrency to sell at current market price, then buying back at a lower price to profit from the difference. | High |

| Margin Trading | Trading cryptocurrencies with borrowed funds, offering potential for larger gains but also greater risks. | Very High |

| Staking | Supporting a network by locking cryptocurrencies to receive rewards, typically in more coins. | Low to Moderate |

| Yield Farming and Liquidity Mining | Lending crypto assets in DeFi platforms to earn interest or rewards, often involving complex strategies. | Moderate to High |

| ICOs and Token Sales | Investing in a new cryptocurrency project’s tokens, similar to crowdfunding, with the hope of value increase. | High |

| NFTs (Non-Fungible Tokens) | Buying, selling, and trading unique digital items or art represented by NFTs. | Moderate to High |

Risks and Challenges in DeFi

While DeFi opens up a world of opportunities, it’s important to understand the risks and challenges involved. As you can see, it’s not just about scams, it’s also about the protocols themselves and how they function.

1) Market Volatility

One of the most noticeable risks in DeFi, and cryptocurrency in general, is market volatility. The prices of cryptocurrencies can swing wildly within short periods. Imagine if your $100 investment suddenly becomes $50 or $150 in a day. That’s the kind of volatility we often see in crypto markets.

2) Security Risks

DeFi platforms run on technology, and like any technology, they can have weaknesses. There have been cases where hackers have found flaws in the code of DeFi platforms, leading to significant losses.

3) Smart Contract Risks

The contracts that run DeFi platforms are called smart contracts. But even smart contracts can have errors or unexpected flaws. If something goes wrong with a smart contract, it can lead to lost funds or other problems.

Sometimes, flaws are built in. Ever heard of a rug pull? A “rug pull” is a term used in crypto to describe a type of scam. In a rug pull, the developers of a crypto project or DeFi platform suddenly take away all the invested money and disappear. This usually happens in projects where the developers have total control over all the funds in the pool, often built into the smart contract (which is why we say it’s so important that the contracts be open-source and audited). Investors are left with worthless tokens, as the developers have withdrawn all the real value for themselves. We’ve put together a guide on how to spot rug pulls, so be sure to check that out if you plan to get involved in DeFi.

4) Liquidity Risks

Some DeFi platforms might not have enough liquidity, which means there might not be enough money on the platform for you to withdraw your funds when you want to. It’s like going to an ATM and finding out it’s out of cash.

Sometimes, this is done intentionally in what’s called a “vampire attack.” A vampire attack is a strategy used by one cryptocurrency platform to drain resources, like liquidity and users, from another platform. This term is unique to the crypto world and is more about competition than actual malice.

Here’s how it typically works: A new DeFi platform offers very attractive incentives (like higher yields or rewards) to entice users to move their funds from an existing platform to the new one. This is often done by creating a similar service or product to the one users are currently using but with added benefits for switching.

The goal of a vampire attack is to quickly grow the user base and liquidity of the new platform by “sucking” these resources from the established platform. It’s a bit like a new coffee shop opening across the street from an old one and offering free coffee for a week to attract customers.

5) Overcollateralization

In DeFi, if you want to borrow money, you often have to provide more in collateral than the amount you’re borrowing. This can be risky if the value of your collateral drops suddenly, as you might need to add more funds to avoid losing it. Imagine borrowing $50 but having to promise $100 worth of your belongings as security.

On the other side of this, it is possible to get crypto loans without collateral. These loans rely on your reputation or credit score in the crypto community and are managed through smart contracts. These loans are riskier for lenders since there’s no collateral to claim if the borrower doesn’t repay, often leading to higher interest rates. However, they are beneficial for borrowers who don’t want to lock up their assets. Some platforms decide who gets a loan based on the borrower’s history and behavior in the crypto community, emphasizing trust and reputation over collateral.

6) Impermanent Loss

For those providing liquidity to DeFi platforms, there’s a risk called impermanent loss. This happens when the price of your deposited assets changes compared to when you deposited them.

7) Lack of Consumer Protection

Unlike traditional banks, most DeFi platforms don’t have consumer protection. If something goes wrong, like a hack or a bug, you might not be able to get your money back.

8) Regulatory Risks

DeFi is still a new field, and governments are figuring out how to regulate it. Changes in laws and regulations can affect how DeFi platforms operate, and in some cases, could even make some aspects of DeFi illegal. It’s like playing a game where the rules suddenly change.

Let’s look at how some of the rules have evolved, and are still evolving.

Regulatory Landscape for DeFi

DeFi exists in a space that’s still quite new to regulators. Governments around the world are trying to figure out how to apply existing financial laws to DeFi or if they need to create new ones.

Unfortunately, different jurisdictions are coming up with different rules, which makes it a little tricky to figure out what to do. If you’re going to use DeFi, we strongly recommend finding out what is legal in your jurisdiction or not.

While they are coming up with different rules, they generally are trying to solve the same problems.

One of the main concerns for regulators is protecting you, the investor. They want to make sure that people don’t lose their money to scams or poorly managed DeFi projects. Protecting investors is a major concern, just like we mentioned in the Lending and Borrowing section above.

Another big focus is preventing illegal activities like money laundering. DeFi’s anonymity features can make it attractive for criminal activities, but we do want to note that most crime still happens in cash, because, as you should know by this point of the article, all activity on the blockchain is public.

Figuring out how to tax DeFi transactions is another issue. Many countries are still deciding how to classify and report earnings from DeFi investments. This makes completing your taxes particularly difficult for those of us investing in DeFi, and especially if we don’t want to break any rules, we need to know what those rules are first.

The biggest challenge is balancing the need for regulation with the freedom to innovate. Too much regulation could stifle the creativity and benefits that DeFi offers. We’ve already seen this problem in the US; regulations in the US are both confusing and restricting, so developers are increasingly moving elsewhere.